Banks sit on one of the most sensitive data ecosystems on the planet. Account numbers, transaction histories, credit scores, behavioral patterns, investment portfolios the kind of information that, if mishandled, doesn’t just hurt a brand. It devastates lives.

Yet as Customer Data Platforms (CDPs) have become central to how banks personalize experiences, run campaigns, and unify customer intelligence, a critical question often gets buried under the excitement of new capabilities: Is this platform actually secure enough to be trusted with banking data?

That’s where SOC 2 certification enters the picture and why it’s becoming a non-negotiable for financial institutions evaluating CDP.

What Is SOC 2, Really?

SOC 2 (System and Organization Controls 2) is an auditing standard developed by the American Institute of Certified Public Accountants (AICPA).

It’s designed specifically to evaluate how technology vendors manage customer data with respect to five Trust Service Criteria:

- Security– Is the system protected against unauthorized access?

- Availability– Is the system reliably operational as promised?

- Processing Integrity– Does the system process data accurately and completely?

- Confidentiality– Is sensitive data protected from unauthorized disclosure?

- Privacy– Is personal information collected, used, and retained appropriately?

Unlike ISO 27001, which is a prescriptive framework, SOC 2 is an audit outcome – a third-party CPA firm examines a vendor’s actual controls and issues a report.

There are two types:

Type I confirms that controls are designed correctly at a specific point in time.

Type II confirms that controls have been operating effectively over a period (usually 6–12 months) – and this is the one that truly matters.

A SOC 2 Type II certification is not a checkbox. It’s evidence of sustained, audited discipline.

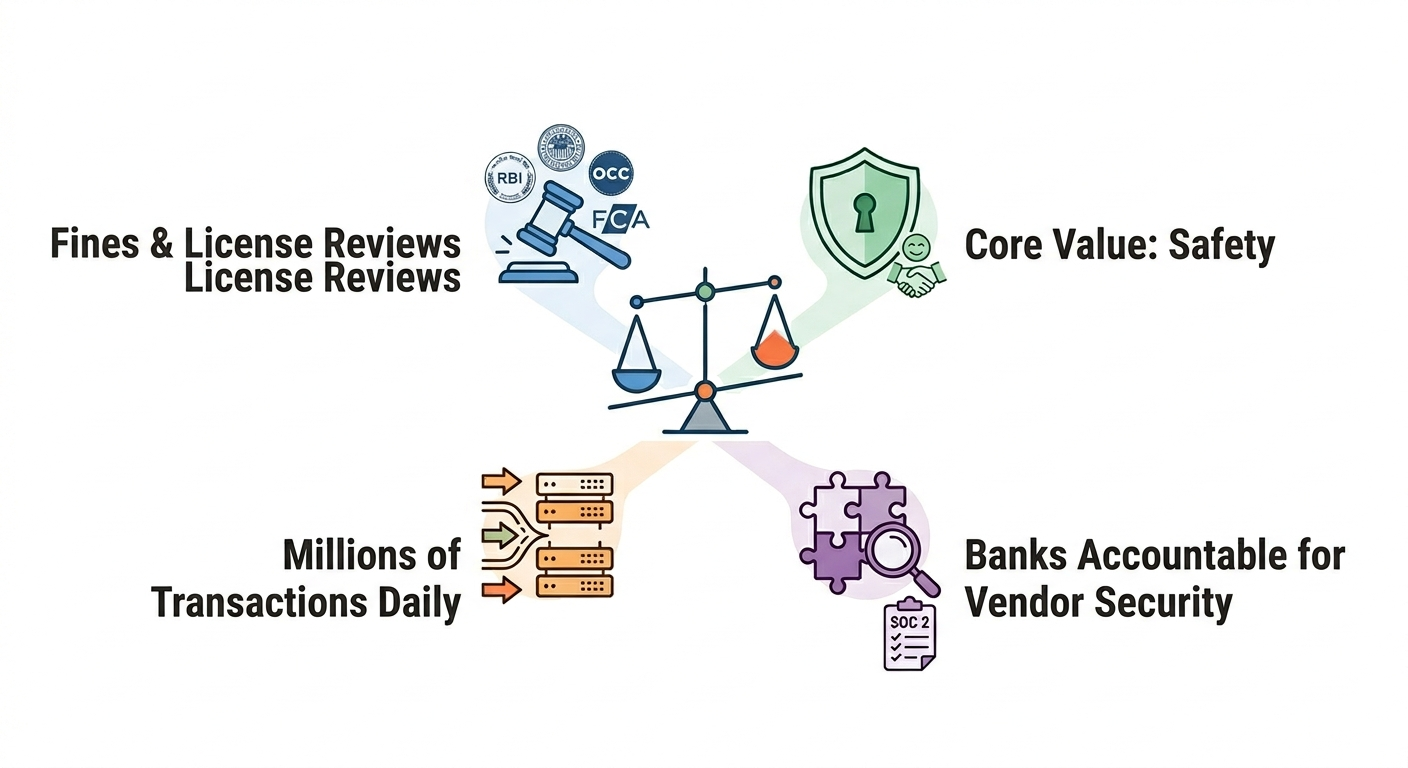

Why Banks Have Uniquely High Stakes

Most industries care about data security. But banks operate under a fundamentally different risk profile:

1. Regulatory exposure is existential:

Banks answer to regulators like the RBI, Fed, OCC, FCA, and others. A data breach tied to a third-party CDP vendor doesn’t just trigger fines; it can trigger license reviews, consent orders, and enforcement actions that threaten the institution itself.

2. Customer trust is the product:

A bank’s core value proposition is safety. If customer data is compromised through a marketing technology vendor, the reputational damage is disproportionate compared to other industries.

3. Data volumes are staggering:

A mid-sized bank running a CDP might be processing millions of transactions, behavioral signals, and identity records daily. The attack surface is enormous.

4. Third-party vendor risk is heavily scrutinized:

Regulators increasingly hold banks accountable for the security posture of their technology vendors. A vendor without SOC 2 certification is a liability that examiners will flag.

What SOC 2 Certification Actually Guarantees in a CDP Context:

When a CDP achieves SOC 2 Type II, it’s confirming several things that matter deeply to banks:

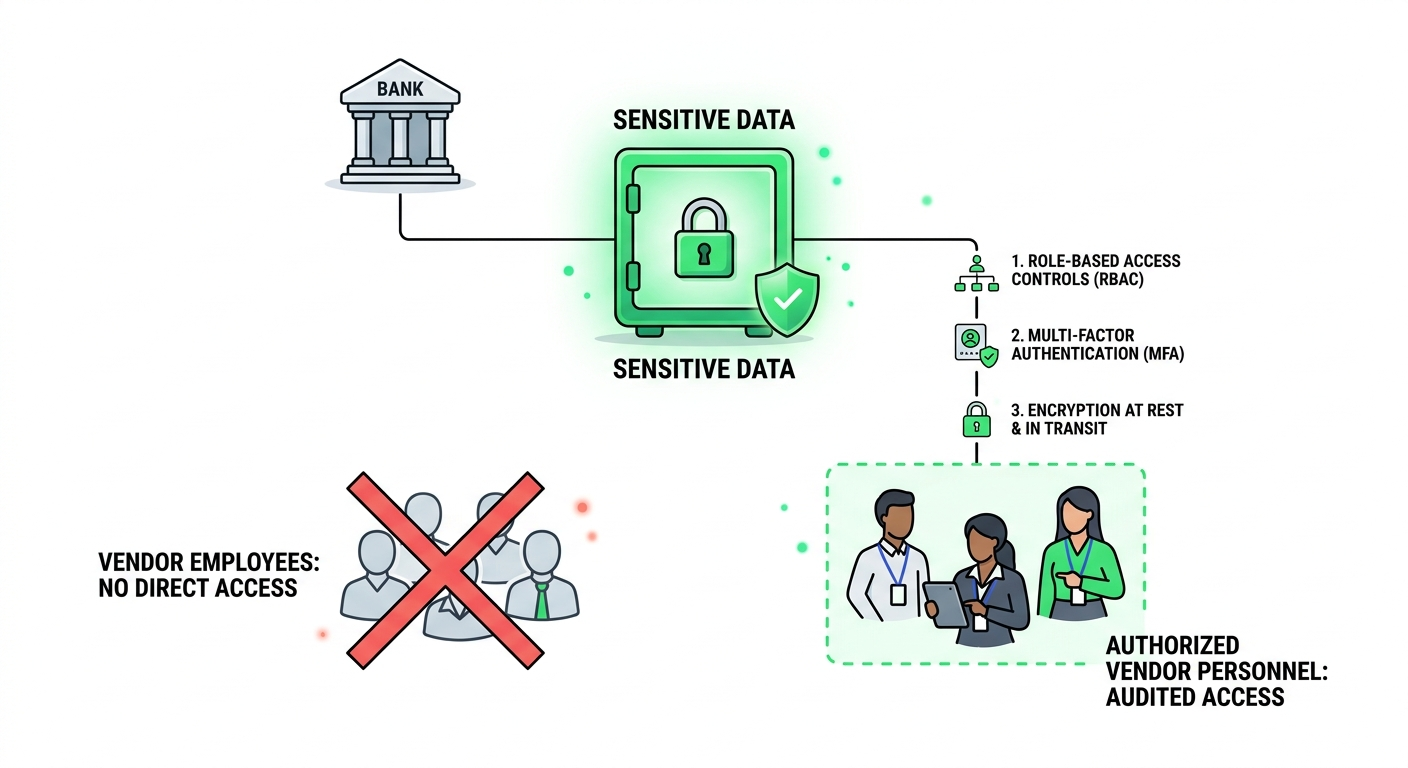

i. Controlled Access to Sensitive Data

The platform has formal, audited processes for who can access what data including encryption at rest and in transit, multi-factor authentication, and role-based access controls. This means the bank’s customer data isn’t accessible to just any employee at the vendor’s company.

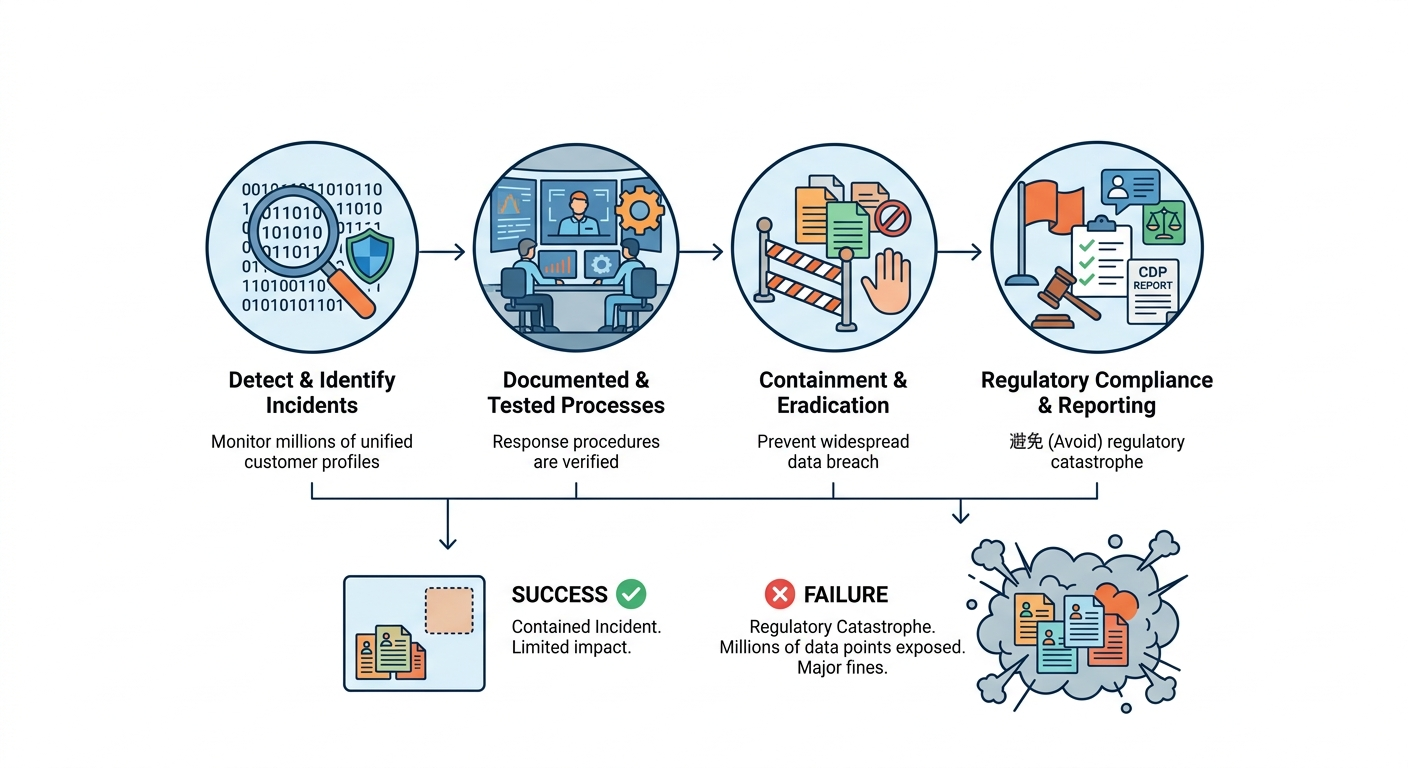

ii. Incident Response Procedures

The vendor has documented, tested processes for detecting and responding to security incidents. For a bank whose CDP might hold unified profiles of millions of customers, this is the difference between a contained incident and a regulatory catastrophe.

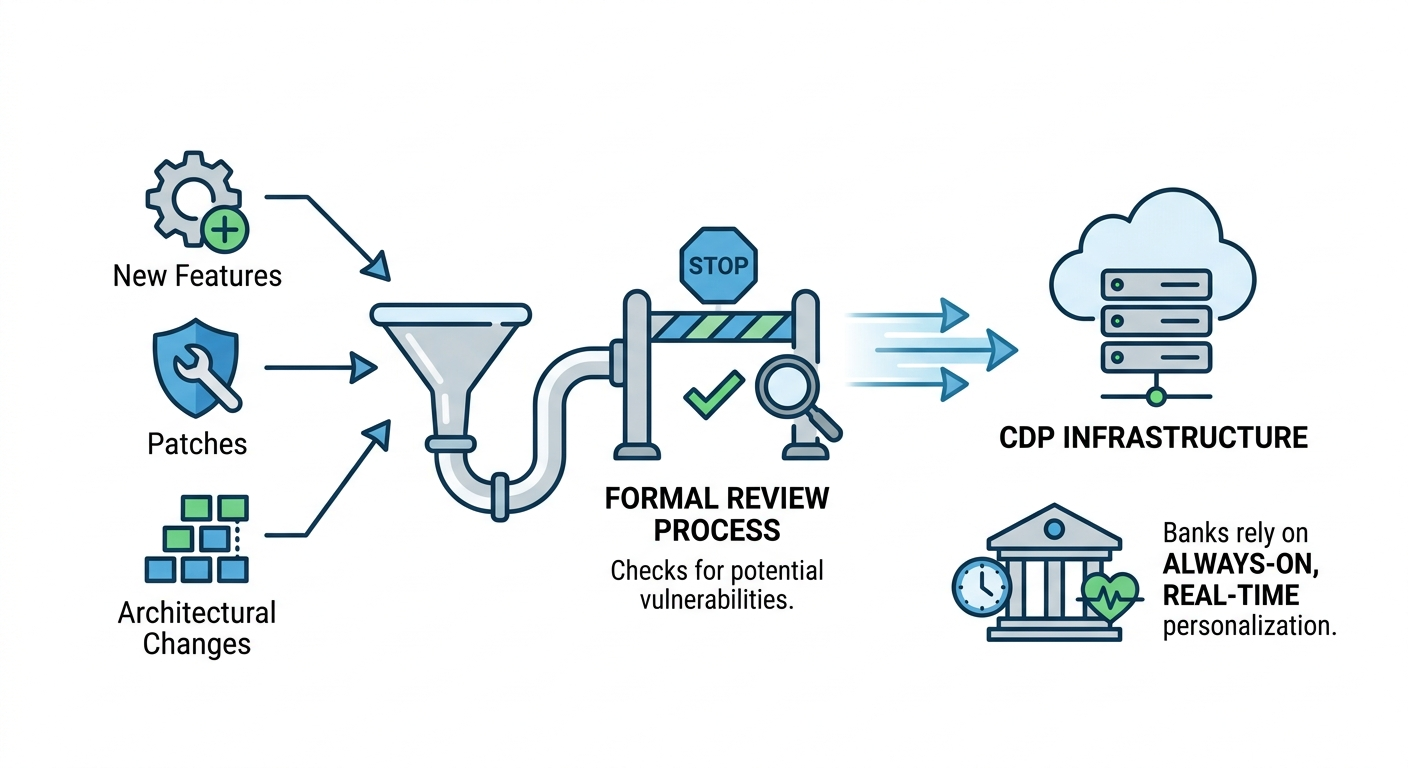

iii. Change Management Controls

Updates to the CDP infrastructure new features, patches, architectural changes go through formal review processes that don’t inadvertently create vulnerabilities. This matters for banks running always-on, real-time personalization.

Updates to the CDP infrastructure new features, patches, architectural changes go through formal review processes that don’t inadvertently create vulnerabilities. This matters for banks running always-on, real-time personalization.

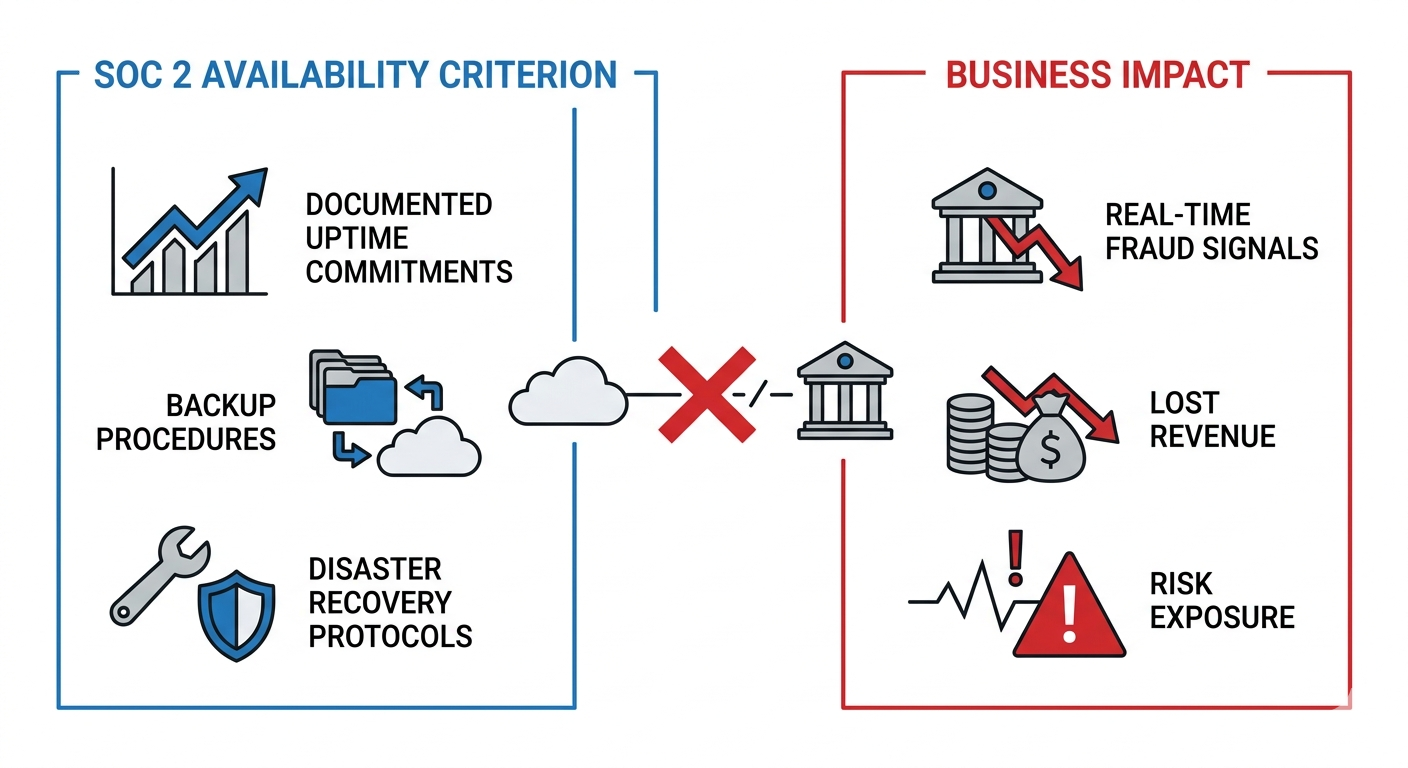

iv. Data Availability Commitments

SOC 2’s availability criterion ensures the platform has documented uptime commitments, backup procedures, and disaster recovery protocols. For banks running real-time next-best-action or fraud signals through a CDP, downtime is directly measurable in lost revenue and risk exposure.

SOC 2’s availability criterion ensures the platform has documented uptime commitments, backup procedures, and disaster recovery protocols. For banks running real-time next-best-action or fraud signals through a CDP, downtime is directly measurable in lost revenue and risk exposure.

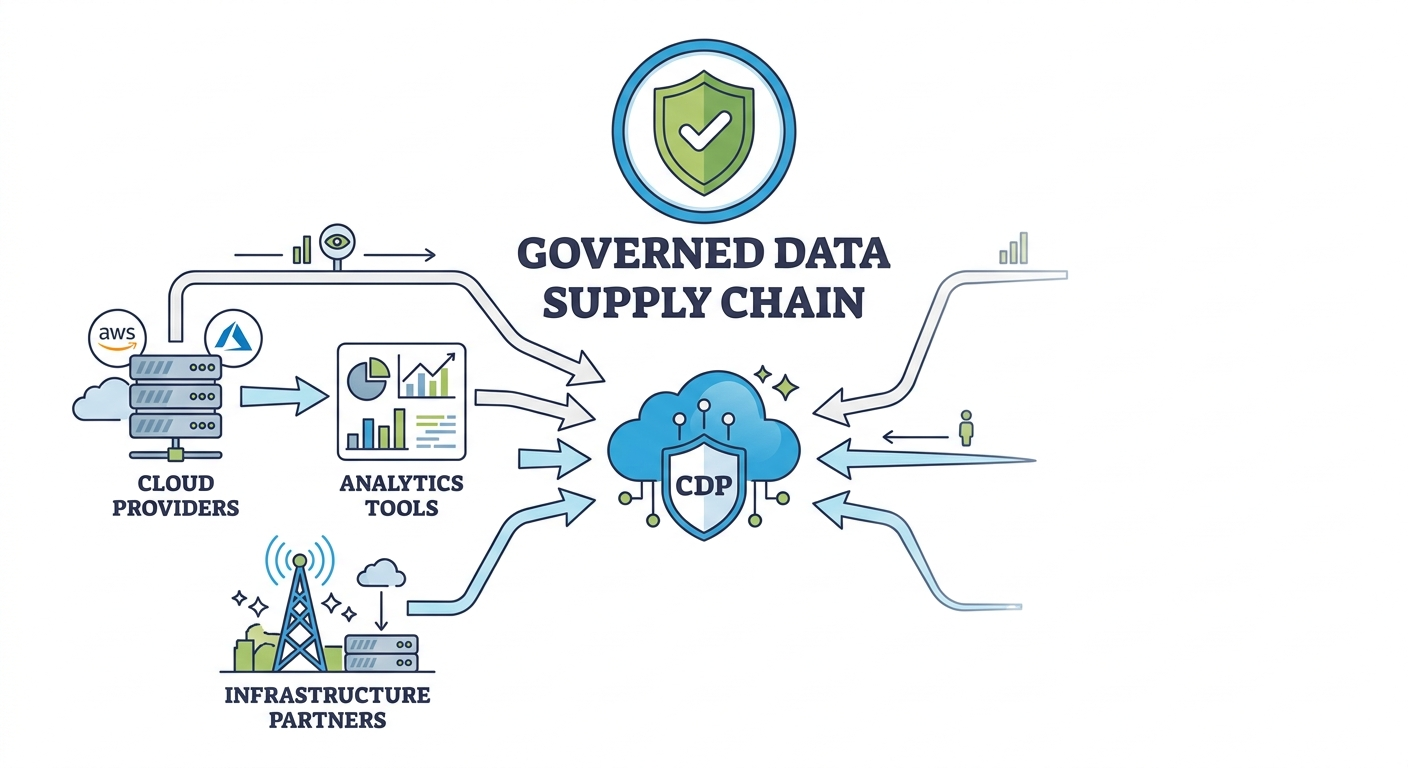

v. Vendor Sub processor Oversight

The audit also covers how the CDP manages its own third-party vendors, cloud providers, analytics tools, and infrastructure partners. Banks need to know that the entire data supply chain is under governance, not just the primary vendor relationship. particularly in low code/API-based ecosystems where multiple integrations expand the data surface area.

The audit also covers how the CDP manages its own third-party vendors, cloud providers, analytics tools, and infrastructure partners. Banks need to know that the entire data supply chain is under governance, not just the primary vendor relationship. particularly in low code/API-based ecosystems where multiple integrations expand the data surface area.

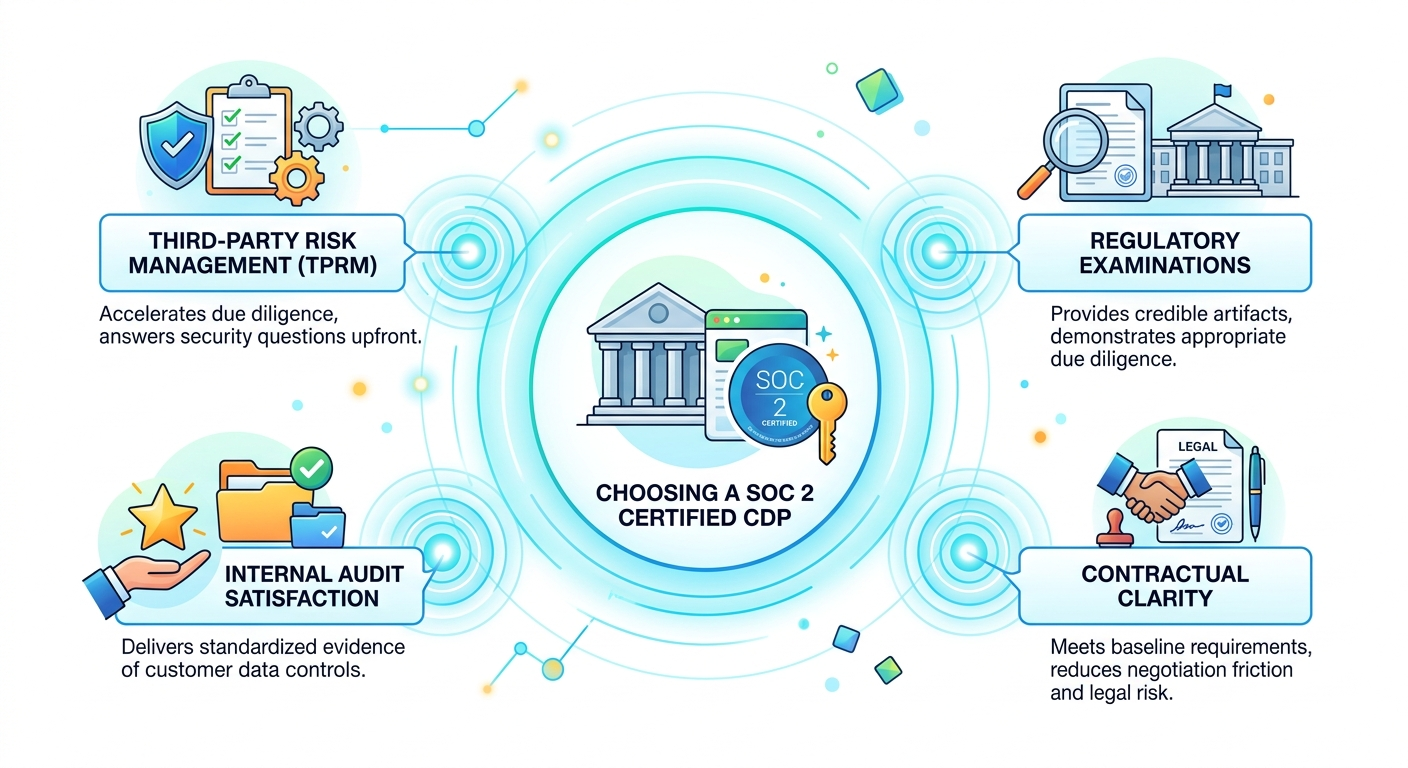

The Compliance Ripple Effect

Choosing a SOC 2 certified CDP doesn’t just protect the bank it simplifies the bank’s entire compliance posture.

Choosing a SOC 2 certified CDP doesn’t just protect the bank it simplifies the bank’s entire compliance posture.

• Third-Party Risk Management (TPRM):

Most banks have formal vendor risk assessment programs. A SOC 2 Type II report dramatically accelerates due diligence. Instead of lengthy security questionnaires and back-and-forth with vendor security teams, a clean audit report answers most questions upfront.

• Regulatory Examinations:

When examiners review technology vendor relationships, SOC 2 reports are a recognized, credible artifact. They demonstrate to regulators that the bank exercised appropriate due diligence in selecting its technology stack. particularly around data privacy and customer data protection

• Internal Audit Satisfaction:

Internal audit teams typically require evidence that customer data handled by third parties is under appropriate controls. SOC 2 provides that evidence in a standardized format.

• Contractual Clarity:

Many bank vendor agreements now require SOC 2 compliance. A certified CDP vendor enters the relationship already meeting baseline requirements, reducing negotiation friction and legal risk.

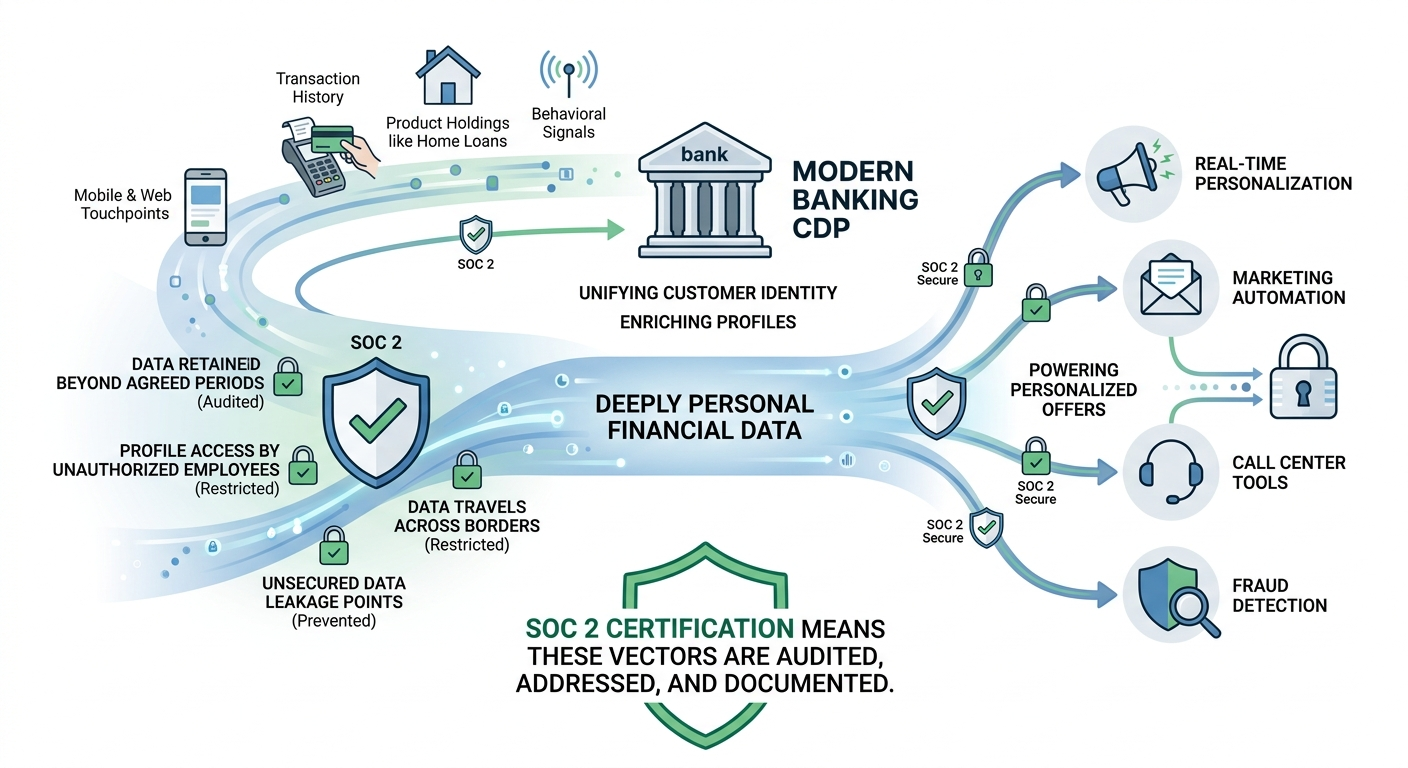

SOC 2 in the Context of Modern Banking CDP Use Cases

Consider what a modern CDP does inside a bank:

Consider what a modern CDP does inside a bank:

- Unifying customer identity across mobile, web, branch, and call center touchpoints

- Enriching profiles with transaction history, product holdings, and behavioral signals

- Powering real-time personalization and audience segmentation for home loan offers, credit card recommendations, and investment nudges

- Feeding downstream systems marketing automation, call center tools, fraud detection platforms

Every one of these activities involves deeply personal financial data flowing through the CDP’s infrastructure. Without SOC 2 controls in place:

- Data could be retained beyond agreed-upon periods

- Profile data could be accessible to unauthorized employees at the vendor

- Data could travel across borders in violation of data residency requirements

- Integrations with downstream tools could create unsecured data leakage points

SOC 2 certification means each of these vectors has been audited, addressed, and documented.

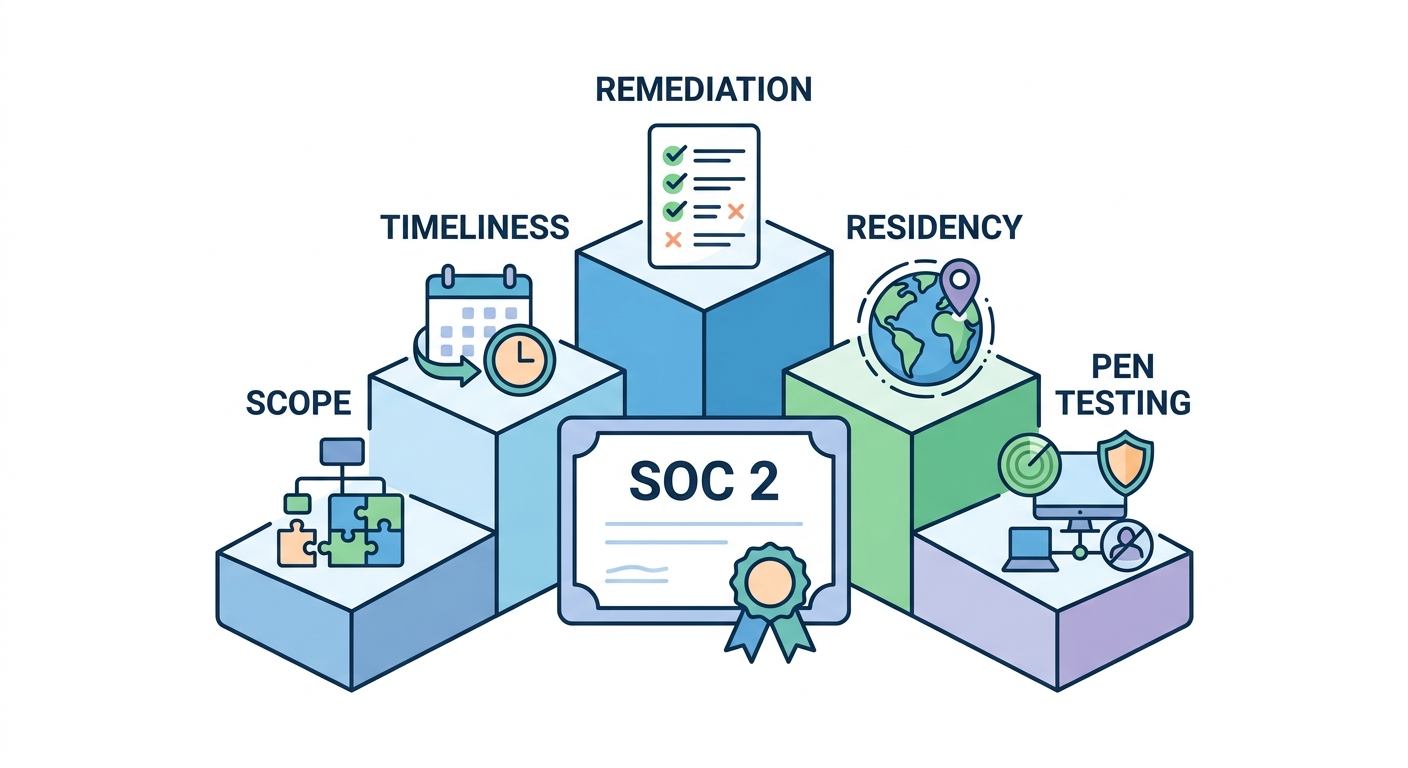

What Banks Should Look For Beyond the Certificate

SOC 2 certification is the floor, not the ceiling. When evaluating a CDP, banks should push further:

SOC 2 certification is the floor, not the ceiling. When evaluating a CDP, banks should push further:

1. Scope of the audit – Does the SOC 2 report cover the specific modules and infrastructure components that the bank will use? A narrow-scope certification may leave critical systems unaudited.

2. Age of the report – SOC 2 Type II reports cover a period in time. A report from 18 months ago provides far less assurance than one from the last quarter.

3. Remediation of exceptions – No audit is perfect. What matters is whether the vendor has documented and addressed any exceptions noted by the auditor.

4. Data residency capabilities – Especially relevant for banks in regulated markets like India, Europe, or the Middle East where data localization laws require customer data to remain within national borders.

5. Penetration testing cadence – SOC 2 doesn’t mandate regular pen testing, but mature vendors do it anyway. Ask for the last pen test report.

6. GDPR / DPDP alignment – For banks operating across jurisdictions, ask how the CDP’s privacy controls map to specific privacy regulations beyond SOC 2’s privacy criterion.

The Cost of Getting This Wrong

Let’s be direct about what happens when banks deploy CDP without adequate security rigor.

In 2023 and 2024, multiple financial institutions faced regulatory scrutiny not because of breaches in their core banking systems, but because of vulnerabilities in their marketing technology stack, including systems supporting real-time predictive scoring and decisioning the very category where CDP lives. Regulators have made clear that “the CDP vendor was responsible” is not an acceptable defense. The bank bears ultimate accountability.

The cost calculus is straightforward: the incremental investment in choosing a SOC 2 certified CDP is a fraction of one percent of the potential regulatory fine, litigation exposure, and remediation cost that follows a serious data incident.

Wrapping Up

For banks serious about data security without compromising on personalization capability, Lemnisk’s CDP is purpose-built for financial services with enterprise-grade compliance at its core.

Lemnisk is SOC 2 Type II certified meaning its security, availability, and confidentiality controls have been independently audited and validated in practice, not just on paper. Beyond the certificate, Lemnisk offers real-time, AI-powered customer data unification across every touchpoint mobile, web, branch, and call center with built-in data residency controls, consent management, and audit trails designed to meet the rigorous demands of banking regulators.

For banks that refuse to treat security and personalization as a trade-off, Lemnisk is the CDP built to deliver both.

Leave a Reply